Market Overview

Central Indiana is comprised of a 9-county region which includes Boone, Hamilton, Madison, Hancock, Shelby, Johnson, Morgan, Hendricks, and Marion counties. Indianapolis, referred to as “Indy”, is the state capital and is the largest city in Indiana. In 1970, the governments of Marion County and the city of Indianapolis consolidated into a city-county form of government. Over the past decade, the Central Indiana area has experienced solid growth and is now home to approximately 2 million residents.

The interconnected highways and railroads around the Indianapolis metro earned Indiana its motto “The Crossroads of America.” Multiple major highways, including I-70, I-69, I-65, and I-74 are linked around Indy by I-465 and provide access to 60% of the U.S. population within a 12-hour drive. National railroads interconnect in multiple areas throughout the city and terminate within a fully secure, international intermodal terminal in downtown Indy. The Indianapolis International Airport adds to the city’s connectivity. The airport is the second largest Fed-Ex air hub in the world and handled over 1 Million metric tons of cargo in 2019, according to the Indiana Economic Development Corporation and Indy Chamber, respectively.

Indianapolis’ connectivity allowed for the growth of its thriving agricultural, life sciences, advanced manufacturing, and technology industries. Central Indiana is home to large corporations including: Eli Lilly (10,005), Roche Diagnostics (4,500), IU Health (23,187), Community Health Network (11,328), Amazon (5,000), FedEx (5,000), Simon Property Group (4,800 in the US), Allison Transmission (2,500), Cummins (58,000 globally), Salesforce (1,700), Infosys (3,000), Rolls-Royce (4,000), and the city (77,249), state (33,520), and federal governments (16,918), per the Indy Chamber. These large employers coupled with the hundreds of thousands of small employers across the 9-county area total over 1 million jobs in Central Indiana. These jobs had an average wage of $54,051 in 2019.

Indianapolis is also called “The Racing Capital of the World.” It’s home to the Indianapolis Motor Speedway which hosts the annual Indianapolis 500 and Brickyard 400. Other magnets for tourism include pro sports teams, like the Indianapolis Colts and Indianapolis Pacers. The Indiana Convention Center also attracts many large conventions such as Gen Con and The National FFA Convention & Expo. Gen Con has about 70,000 attendees and a $70 million economic impact. It’s the largest event hosted by the Convention Center, according to the Indianapolis Business Journal. The Children’s Museum of Indianapolis consistently ranks within the top museums to visit in the country and in North America. In 2017 there were 28.8 million visitors to Central Indiana who supported the $5.4 billion tourism industry.

Indiana also houses multiple world-class universities with high-ranking programs. Several of these are in Indianapolis or are located within an hour and a half drive: Indiana University – Purdue University Indianapolis (IUPUI) (34,699 students), Indiana University – Bloomington (46,723 students), Purdue University (46,806 students), Rose-Hulman Institute of Technology (2,313 students), Butler University (5,306 students), Marian University (4,449 students), University of Indianapolis (6,830 students), and Ball State University (27,369 students). According to the U.S. News and World Report, 2020 edition, Purdue has the #1 Undergraduate and Graduate Biological/Agricultural Engineering Program, Indiana University has the #1 Graduate Public Affairs Program, Butler University is the #1 Regional College in the Midwest, and Rose-Hulman has the #1 Undergraduate Engineering Program (where no doctorate is offered) in the United States. These universities help feed the employment need in Central Indiana.

The Indiana Economic Development Corporation states that Indiana is ranked first in State Infrastructure (CNBC 2019), first in number of pass-through highways (IEDC), second in Best States for Long-Term Fiscal Stability (US News and World Report, 2018), second in Property Tax Index (The Tax Foundation, 2019), and in the Top 5 U.S. States for Business (Chief Executive, 2019). Central Indiana is home to suburban cities who maintain high rankings in quality of life. Fishers, a booming tech hub, ranked third in MONEY’s Top 10 Best Places to Live in 2019. Carmel, an arts, culture and entertainment hub ranked first in Niche’s Best Places to Live in Indiana in 2020, 2019, and 2018. Central Indiana is filled with vibrant companies, cities, and citizens.

Population

2,034,728

Households

790,307

Median Household Income

$61,305

Education

27% Highschool

27% Some College

36% Bach/Grad+

Total Businesses

66,206

Total Employees

1,011,041

Source: Esri

Industrial OVerview

MOMENTUM CONTINUES INTO Q1 2021 WITH CONTINUING DEMAND, ESPECIALLY IN DISTRIBUTION AND LOGISTICS

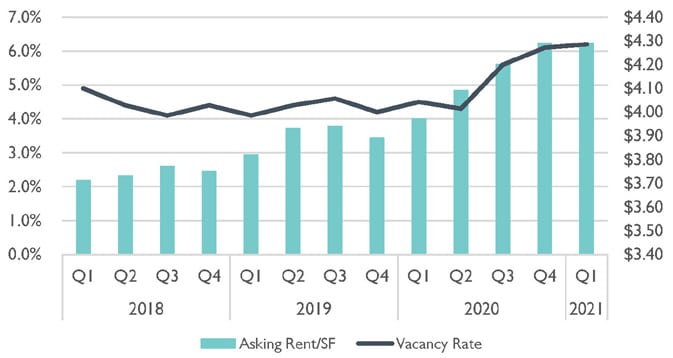

Thanks to Indianapolis’ connectivity that includes interstates, rail lines, and the second largest FedEx hub, the Indianapolis metro continues to be in high demand for warehouse and industrial users. The Indianapolis market consists of 31 concentrated areas with over 320.7 million square feet of industrial / warehouse space. Currently in 2021 there is over 7.75 million square feet of space under construction and 2.6 million square feet completed year to date. CoStar reported at the end of Q1 a vacancy rate of 6.2% which is an increase from the end of Q4 2020 of 6.1%. Demand for industrial property is keeping average asking rents relatively high. The asking rent per square foot stayed at $4.29 between Q4 2020 and Q1 2021, which is 8.06% higher than Q1 2020.

Nationwide, industrial product continued to be in demand throughout 2020 and shows no sign of slowing down in Q1 2021. The Indianapolis metro is a strong market, especially for distribution and logistics. Several new projects have been announced.

- Electrical Repair & Maintenance Co. Inc., or ERMCO, who is based out of Indianapolis, has released plans to build a new 205,220 square-foot headquarters in Greenwood. The plans include 63,240 square feet of office and 141,980 square feet of shop space and storage. These plans will bring 170 jobs to the Southside of Indianapolis and is projected to be completed in the fall of 2022.

- Apple Inc. announced plans to invest $100 million for a new facility in Clayton, in Hendricks County. The project will create nearly 500 jobs by the end of 2024. XPO Logistics Supply Chain will operate the high-tech distribution center. A construction timeline hasn’t been released yet.²

- Bobby Rahal announced a $20 million investment to build a 100,000 square-foot building in Zionsville. This will consist of office space, research and development and light manufacturing.

- Style Link Logistics LLC announced plans to invest $3.5 million in Whitestown to open a new facility that will employ 500 workers. The facility size has not been reported but will be located in the 65 Commerce Park Building.³

Trends

- The Indianapolis metropolitan area had positive, but moderate employment growth with 1,500 new jobs added during Q1 2021, which was a growth rate of 0.1%.

- Leasing activity generated 2,034,074 square feet of absorption during Q1 2021. Over the last 12 months, market absorption totaled 6.96 million square feet, 4.13% lower than the average annual absorption rate of 7.26 million square-feet.

- Higher construction costs will factor into future rents as new buildings hit the market.

INDUSTRIAL ASKING RENT & VACANCY

Source: CoStar

INDUSTRIAL ABSORPTION TRENDS

Source: CoStar

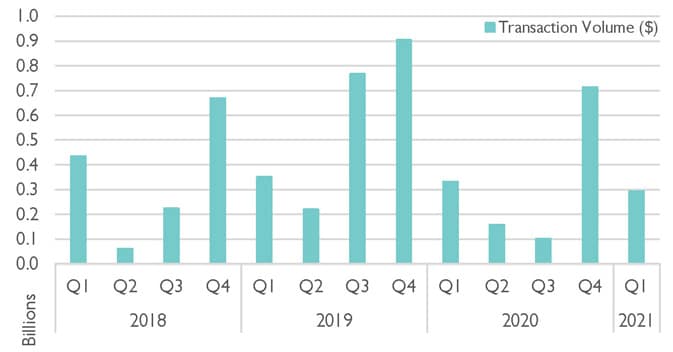

INDUSTRIAL SALES TRANSACTION VOLUME ($)

Source: Real Capital Analytics

Office Overview

OFFICE IS EMERGING FROM ITS HOLDING PATTERN AND IS SET FOR MORE ACTIVITY NOW AND IN THE FUTURE

The Indianapolis office market is comprised of 37.8 million square-feet in 20 geographic concentrations. The Q1 2021 vacancy rate for Indianapolis was 17.7%, a 70 basis-point increase from Q4 2020. The Q1 average asking rent in Indianapolis was $20.84 per square-foot. This is an increase of 0.77% from Q4 2020 and a 3.27% increase from Q1 2020.¹ Asking rent is expected to fall 1.8% by year end. Effective rents are expected to decline 4.1% in 2021 and rise 0.6% in 2022. Vacancy rates are expected to increase in the near to mid-term due to soft market fundamentals.²

Notable buildings under construction include:

| Location | SF | Completion | |

|---|---|---|---|

| First Internet Bank HQ | Downtown Fishers | 168,000 | Fall 2021 |

| Zotec Partner's HQ | Carmel | 120,000 | Late Q2 / Early Q3 |

| The Union 601 | Downtown Indy | 66,000 | Late Q2 / Early Q3 |

Notable deliveries of office buildings include 16 Tech’s HqO downtown Indianapolis. The 54,000 square-foot building had its grand opening in early April.³

Pennwood Office Park (72,850 s.f.) was a notable sale at $8,650,000 in the North/Carmel submarket.²

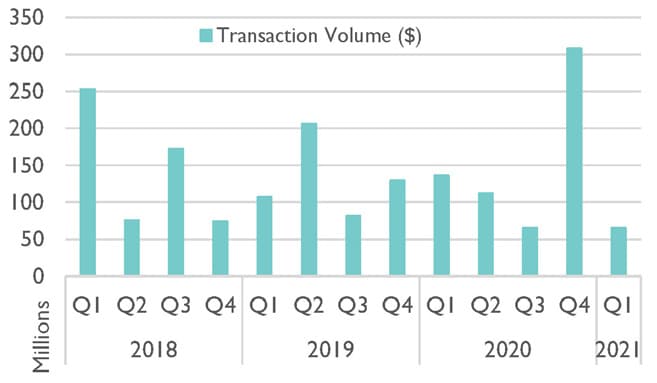

Year-over-Year sales volume was down 52.3% in Q1 2021. This is most likely due to many properties being sold in Q4 2020 (positive sales volume increase of 138% YOY).⁴ Sales volume was also down in Q1 because of a low supply of properties for sale that potential sellers might want for a 1031 exchange.⁵

Landlords and tenants are transitioning out of their “wait-and-see” mode as vaccines are rolling out and companies are completing evaluations of their space needs. It’s currently a tenant’s market and landlords are making concessions to get their space occupied. Concessions include high tenant improvement dollar amounts and long free rent periods. However, landlords are protecting the value of their assets by keeping face rents at historically high levels.⁵

Due to the current recession, tenants are more conservative with the amount of money they spend on rent and are downsizing their office space to avoid downsizing their workforce. Tenants are also using landlord’s tenant improvement dollars to upgrade their space to fit their needs. The pandemic caused tenants to take creative measures to use their space by utilizing remote working and hoteling. These approaches to office space depend on the size of the company because larger corporations look at office space differently.⁴ Consulting firm KPMG conducted a survey of over 500 CEOs of large, influential companies in February and March 2021. They reported that 17% of the companies say that reducing their physical footprint is in their plans. This percentage is down from the August 2020 number of 69%.⁶

There are still office spaces available for sublease, however, the amount of square feet available is not as high as expected.⁵ In popular locations, like Keystone at the Crossing, space available for sublease is receiving multiple offers within a short timeframe while less in-demand locations are staying on the market longer. Additionally, smaller spaces available for sublease with relatively short terms under 5 years, are leasing faster than larger spaces with longer lease terms.⁵

Trends

- The number of lease transactions will continue to increase as the economy comes out of the recession and as more leases expire. The timeline for change in the office market is longer than other product types due to the longer average contract length.

- Indianapolis is projected to have a 2.2% total job increase in 2021, this is the beginning of a job recovery from 2020 where there was a decline of 1.7% in total jobs (18,300 jobs) in Indy. The city should recover all its lost jobs by 2022.2

-

The annual net absorption for 2020 was negative and is expected to remain negative in 2021. Inventory is expected to increase with the delivery of multiple developments within the year. This will most likely increase the vacancy rate near year-end 2021.2

Sources

- CoStar

- Moody’s Analytics REIS

- Inside Indiana Business

- Real Capital Analytics

- Bradley Company

- KPMG

OFFICE ASKING RENT & VACANCY

Source: CoStar

OFFICE ABSORPTION TRENDS

Source: CoStar

OFFICE SALES TRANSACTION VOLUME ($)

Source: CoStar

Retail Overview

RETAIL IS STILL STRUGGLING BUT NEW CONCEPTS AND INDEPENDENT QUICK-SERVE RESTAURANTS ARE ACTIVELY EXPANDING

During Q1 2021, the Indianapolis metro’s asking rent increased from $13.27 in Q4 2020 to $13.50 in Q1 2021. Net absorption stayed positive between Q3 2020 and Q1 2021. The net absorption for Q1 was 375,652 square-feet. The vacancy rate for all types of retail property in Indianapolis increased to 5.0% in Q1 2021 from 4.8% in Q4 2020 according to CoStar data.¹

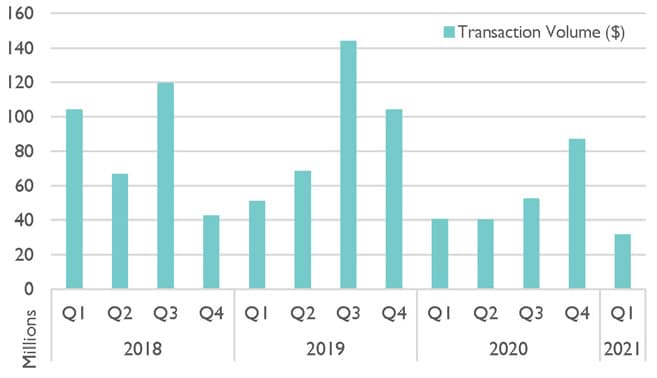

Per Real Capital Analytics, notable sales include 17535 Terry Lee Crossing (11,314 s.f.) for $4,480,155 and Stafford Crossing in Plainfield (26,510 s.f.) for $4.9 million. Total sale transactions for Q1 2021 equal $31,342,917, which is a negative 21.7% year-over-year change. Total square-feet sold in Q1 was 513,819, which is a positive 0.2% year-over-year change. The average price per square-foot is $61 year-to-date, a negative 53.1% change year-over-year and the average cap rate was 7.5%, a negative 40 bps change year-over-year.³

A good portion of activity in the retail sector is coming from independent quick-serve restaurants, medical users, financial services, and fitness concepts. Landlords are giving tenants free rent in lieu of tenant allowance to keep up the value of their properties. The suburbs and some downtown locations are seeing increased leasing activity.

The trend for medical office tenants to move into traditional retail space and build it out continues. With traditional retail hampered by the effects of the Coronavirus pandemic and the increase in e-commerce, property owners are using healthcare to fill vacant spaces.⁴ The pandemic most likely accelerated this trend, as well as the adoption of telehealth.⁴ Telehealth is now projected to grow 10-15% per year.⁵ The amount of square feet for administrative space needed by medical practitioners is projected to decline while clinical space has a foggier future.⁵ Industry experts believe that the amount of clinical space needed may stay the same or even expand due to physicians’ increased ability to reach out to rural populations.⁴ This means that the amount of retail space needed by medical tenants may expand.

Traditional retailers are continuing their 2020 trend of exiting enclosed malls and opening off-mall locations. Some of the reasons cited for moving include lower rents, flexibility of operating hours, and ease of parking. Bath & Body Works found that their conversion rates for customer sales was two times higher in locations other than enclosed malls. Other specialty shops also moved out of malls, reducing the tenant mix, which hindered demand.⁵

One of the largest malls in Central Indiana, Circle Center Mall, recently saw a switch in management companies. Simon Property Group had managed the mall for 26 years before handing management off to JLL. Simon will retain partial ownership and leasing of the mall.⁷ This may signal a coming change to the mall as it struggles through the pandemic, which led to few office workers and tourists in downtown Indianapolis.

Trends

- The Restaurant Revitalization Fund that gives restaurants access to $28.6 Billion in grants will help keep some restaurants afloat, but not all.8

- Traditional retail spaces will likely see the continued trend of medical users filling vacant space. Higher vacancy rates in can be used to help the healthcare client negotiate a rent rate better than those found in traditional medical office buildings, and retail is traditionally located in easily-accessible areas.

- The trend of big box stores being transformed into new uses will continue into the foreseeable future, partly driven by the shortage of Industrial space.

- Vacancy rates are projected to decrease as leasing activity begins to accelerate.

Sources

- CoStar

- REIS

- Real Capital Analytics

- RE Journals

- Globe Street

- IBJ

- CBS 4 Indy

- Restaurant Dive

RETAIL ASKING RENT & VACANCY

Source: CoStar

RETAIL ABSORPTION TRENDS

Source: CoStar

RETAIL SALES TRANSACTION VOLUME ($)

Source: CoStar